Colesworth, when duopolies backfire

The real story behind how Australia's supermarkets came unstuck

When the Federal Court ruled last week that Coles’ “Down Down” promotion was in fact a scam, this was, on the face of it, a simple example of a regulator applying the rules and making a case stick. It was actually a far more intriguing and nuanced case of societal forces cascading into what could well be a record fine north of $100 million dollars.

If you are an Australian grocery shopper, that very first force was one you had in your gut in 2024, when Coles and Woolworths announced record profits while prices had exploded and real wages declined. It was a feeling of betrayal between these businesses and a very key stakeholder group, their customers (most likely you).

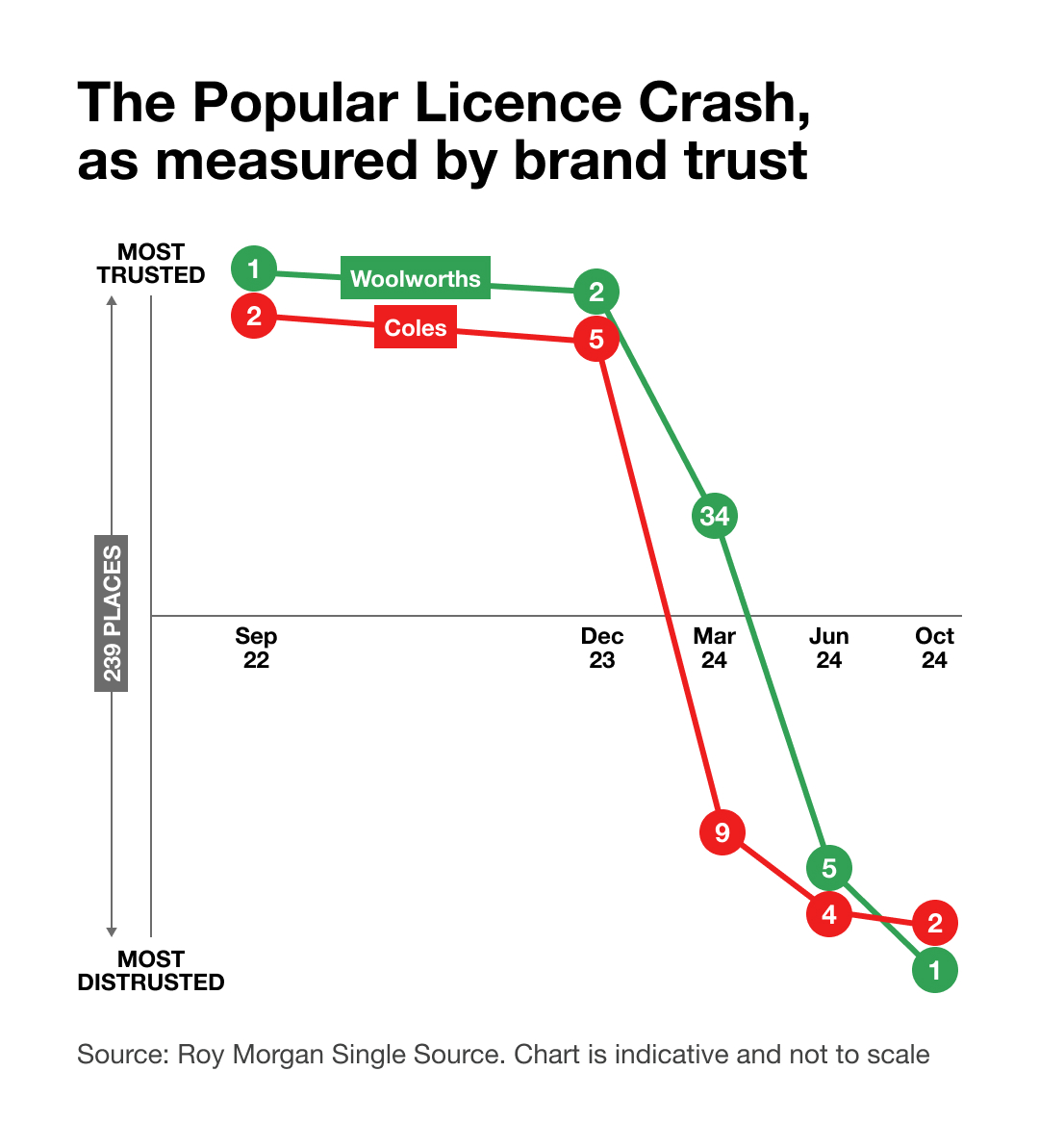

COVID had placed Coles and Woolworths at the centre of Australian life. Both were classified as essential services and remained open while other retailers closed. Their CEOs became public faces of pandemic continuity. By the end of 2021, both companies sat near the top of Roy Morgan’s national trust rankings, with Woolworths inside the top three most trusted brands and Coles inside the top five.

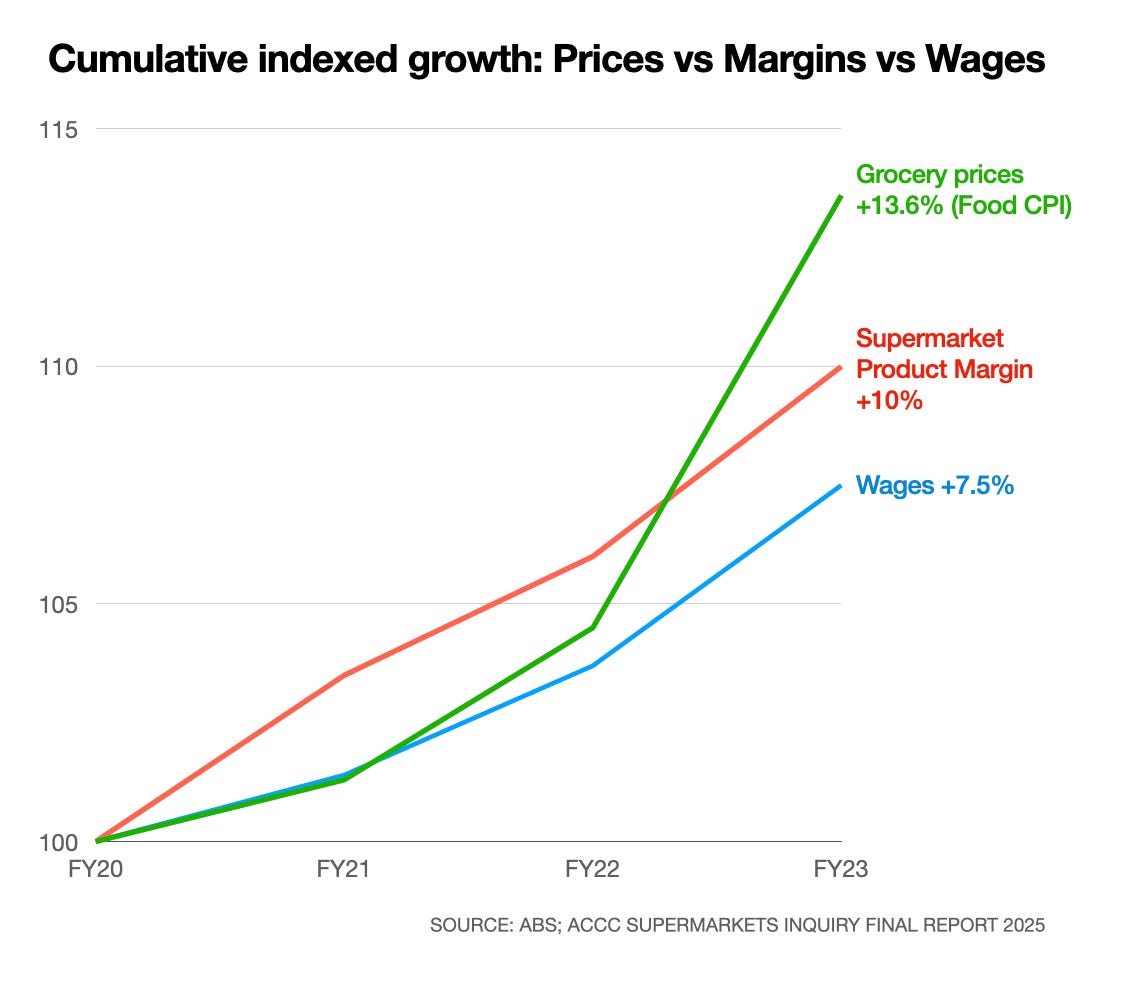

The ACCC’s final supermarket inquiry report, released in March 2025, documented what followed. Grocery prices rose approximately 24 per cent across the five years to mid 2024. Coles’ and Woolworths’ product and EBIT margins expanded during the same period. Between late 2022 and early 2023, grocery prices rose at more than twice the rate of wages. The regulator stopped short of finding price gouging, but the structural picture was unambiguous, margins moved up while household purchasing power moved down.

There are three types of societal forces, or “licences”, that businesses operate under.

In a competitive market, your feelings of betrayal would normally be limited to a hit on an organisation’s Social Licence, as you are just one of their stakeholder groups, a customer. Your dissatisfaction expresses itself by shifting share to alternatives, and the issue resolves through commercial competition.

In a duopoly, the picture is different. When two operators serve approximately 65 per cent of a market, the customer base and the general population are substantially the same group. Social Licence damage to customers becomes Popular Licence damage by definition, because the customer is the public.

This is a structural feature of the Australian economy. Banking, energy retail, domestic aviation, and telecommunications all run on duopoly or near-duopoly structures. In each, the customer is also the citizen, the voter, the talkback caller, the social media poster.

Stakeholder friction does not stay contained in the Social Licence. It instantly propagates into Popular Licence damage, and into Public Licence (regulator and lawmaker) consequences faster than it would in a market with five or six credible operators.

Crystallisation

The fundamental damage to the two supermarkets’ Social and Popular Licences could already be seen in the brand trust scores at the end of 2024. What happened next was a series of events that supercharged and focused it into a pressure that politicians and regulators could not ignore.

The Popular Licence damage compounded across 2024. In February, the Four Corners episode “Super Power” named eight structural tactics. Supplier squeeze, market concentration, phantom brands, land banking, restrictive contracts, promotional rebates, misleading discount tickets, and shrinkflation. None of these tactics were new but the programme made them visible to a population already attuned to receive them. Brad Banducci walked out of his interview on camera, and the clip ran in national news cycles for more than a week.

In April, the Senate Select Committee threatened Banducci with contempt. Senator Nick McKim’s accusation, that Woolworths had used market dominance to squeeze suppliers, force down wages, compromise staff safety, and price gouge customers, packaged the cumulative critique into a single sentence in Hansard.

By November, the Australian National Dictionary Centre had named “Colesworth” the 2024 Word of the Year. Roy Morgan ranked Coles and Woolworths as Australia’s two most distrusted brands, displacing Optus. The trust position both companies had earned during the pandemic had inverted within a single year.

The Public Licence cascade

Once the Popular Licence damage had compounded to that point, the Public Licence consequences were inevitable. Regulators, parliament, and ultimately the courts arrived in sequence.

The ACCC filed Federal Court action against Coles and Woolworths in September 2024, alleging that approximately 245 Coles products and 266 Woolworths products had been sold under misleading “Down Down” and “Prices Dropped” discount tickets between 2021 and 2023. The conduct alleged had been operating for three years, what had changed was the Popular Licence context.

The Emerson Review of the Food and Grocery Code, handed down in June 2024, recommended making the previously voluntary code mandatory, with maximum penalties of $10 million per breach. The Government accepted all 11 recommendations. The mandatory code took effect in February 2025.

In December 2025, Parliament passed the excessive-pricing law, banning excessive pricing by supermarkets with revenue above $30 billion. Only Coles and Woolworths qualified, with penalties up to $10 million per breach. The legislation passed *despite* the ACCC’s own final supermarket inquiry report, handed down in March 2025, not finding evidence of price gouging. In politician’s eyes the regulator was overruled by Popular Licence.

The Federal Court ruling last week is the final Public Licence consequence in the sequence. Justice O’Bryan’s finding that Coles’ “Down Down” promotions were misleading on 13 of 14 sample products sets a new precedent. The 12-week was-price rule he established applies to every retailer in Australia using was-now promotional pricing.

Lessons

The internal reviews into why Coles and Woolworths could be exposed to hundreds of millions in fines will have no shortage of culprits. Everything from deficient corporate governance of pricing promotions, to legal strategy, global supply chains, and irascible CEO media performances.

All, and more, will be contributors, but the true fundamental cause of the finding was an underestimation of dynamics between their societal licences (social, popular, public) and the lack of an informed plan to harness them.